2024-10-29 17:47:32 :

The name was partly inspired by a trip to Everest Base Camp by Managing Director Mohit Bhatnagar, one of the three longest-serving members of Sequoia India, who was also inspired by the “climb.” Inspired by the mountaineering philosophy of “go high, sleep low”. The idea is to allow the body to adapt to the environment rather than suddenly doing something risky.

But the new name has not yet been announced.

Instead, the venture fund’s brand value appears to have eroded since losing its Sequoia moniker. Earlier this month, the fund’s general partners decided to reduce compensation at its growth fund, a move likely prompted by this stark reality. At a time when most global investors are bullish on India, the 16% ($465 million) cut from its current $2.85 billion fund, earmarked for seed, venture and growth stage deployments, also surprised observers.

In addition to all of this, the investor has encountered a number of other issues over the past few years, not least the exposure of its portfolio companies to a host of corporate governance issues.

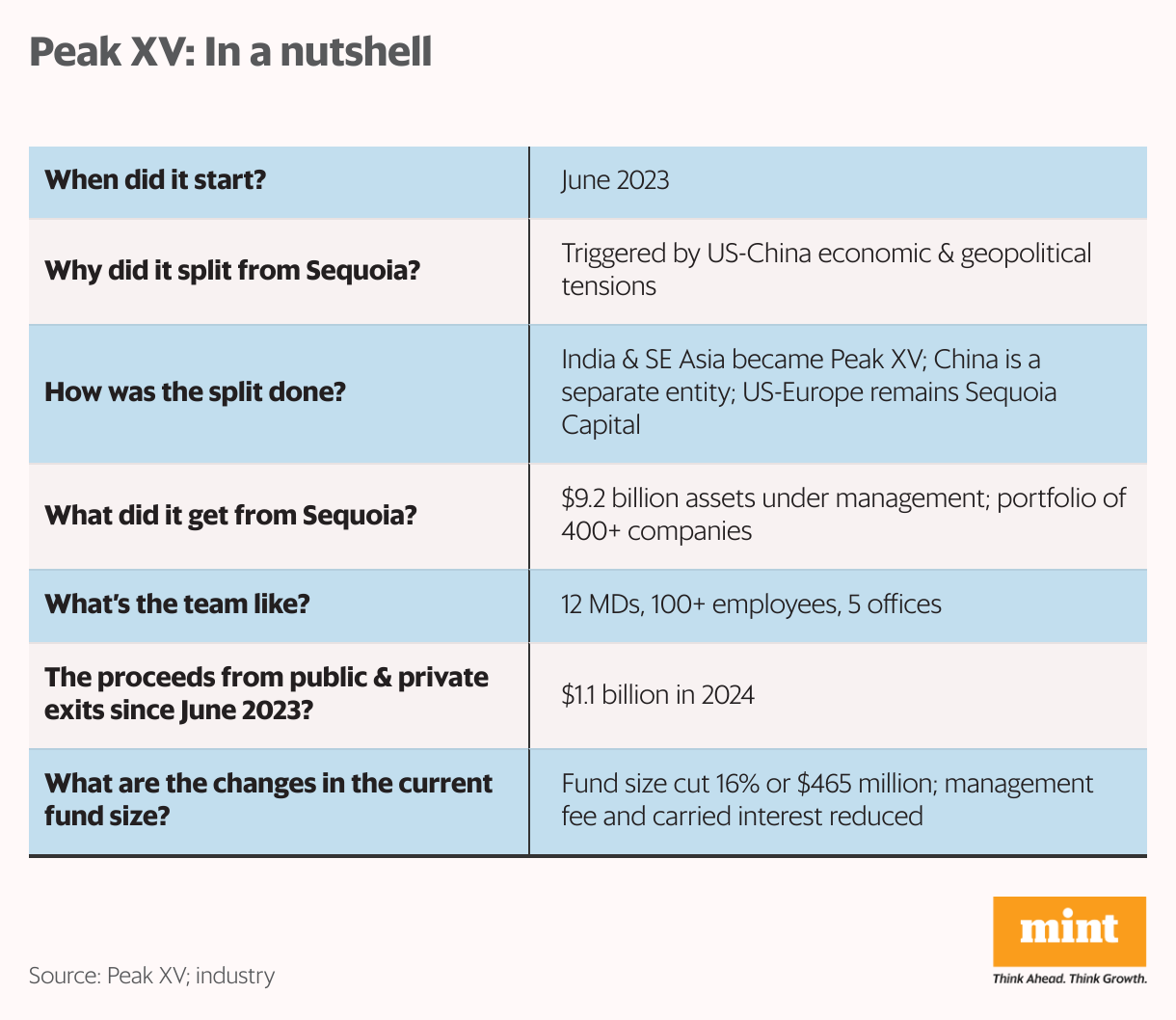

Still, Peak XV has a lot going for it, having inherited $9.2 billion worth of assets under management from Sequoia India, spanning a portfolio in India and Southeast Asia. Over the past 18 years, Sequoia has invested in 400 companies in these two regions (South Asia). East Asia accounts for a quarter of the business through 13 funds.

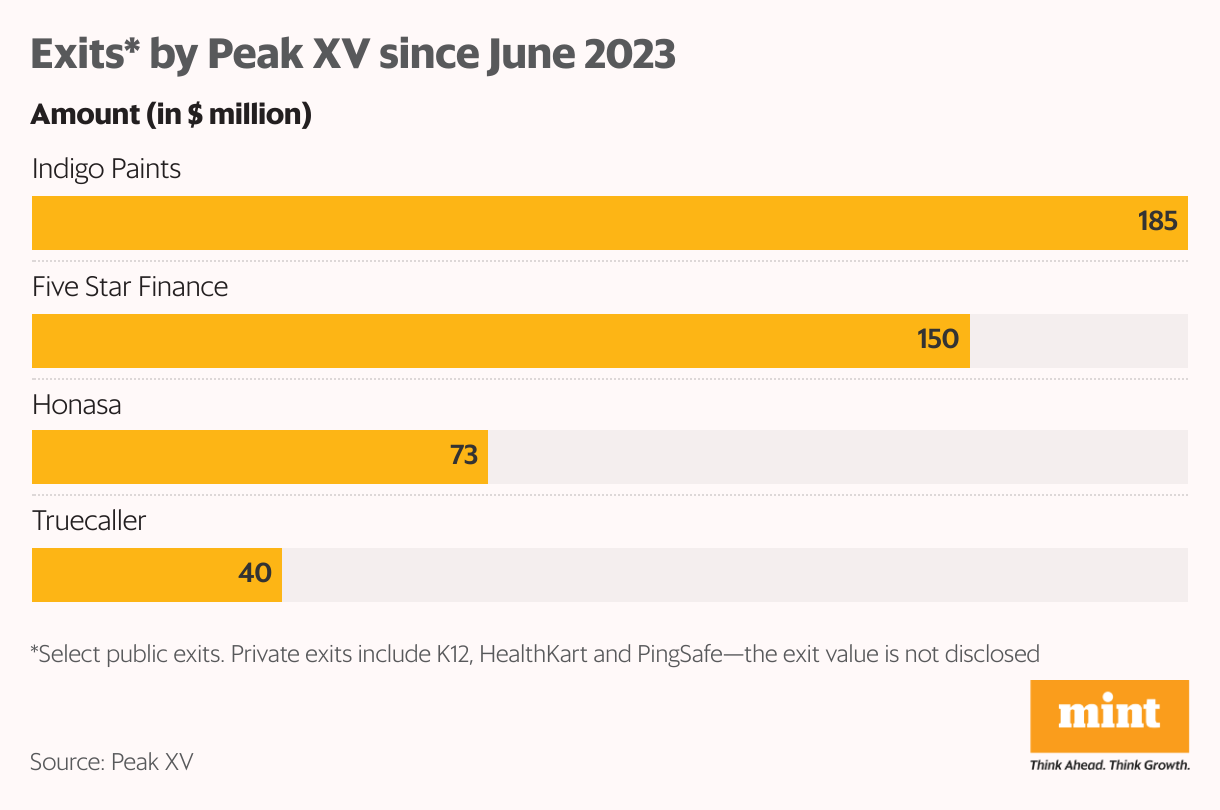

The portfolio, inherited by Peak XV Partners, includes Zomato, Truecaller, Pocket Aces, Absolute Foods, Atlan, Pine Labs, Cred and Groww. The last three are expected to be listed in early 2025, and another 23 companies have already been listed. In fact, Peak XV has facilitated more IPOs than any other India-focused fund. Since the rebrand in June 2023, portfolio companies have generated $1.1 billion worth of public and private exits.

The venture capitalist’s portfolio includes 44 companies with revenue in excess of $100 million and 70 companies with revenue in excess of $50 million. “These indicators will determine our exit,” Bhatnagar said.

The holding fee is shocking

Earlier this month, Peak XV made a surprising announcement. The venture fund’s leadership’s decision to lower management fees and earn interest on its growth and multi-level funds is the clearest sign that as the Sequoia name disappears, so does the premium they enjoyed. The reduced fees are in line with those of other funds in India.

A venture fund’s management fee is an annual fee that is used to compensate the fund’s general partner (GP) for the work it does and to cover expenses incurred in operating the fund, such as salaries, rent, travel, insurance and other administrative expenses. Fees are typically based on a percentage of the fund’s committed capital, but can also be based on a percentage of the fund’s returns or assets under management. Typically, general partners charge a management fee of 2% to 2.5%. Peak XV took the unusual step of lowering management fees and carried interest from 2.5:30 to 2:20.

The fact is, when our cost of capital is higher than other companies, it actually makes us uncompetitive. ——Shailendra Singh

Carried interest, or “carried interest,” is what general partners receive when they identify and invest in businesses that may become large companies in the future. The “spread” is a portion of the fund’s profits and is a performance-based incentive designed to ensure that the interests of the general partner are aligned with those of the fund’s investors (limited partners or limited partners). If the spread is 20%, the GP will receive 20% of any investment profits after the principal is returned to the LP. The remaining 80% is owned by LP. So, in absolute terms, if a fund earns $10 million in annual profits from its principal investment (for example, investing $1 million in a business), $1.8 million goes to the general partner and $7.2 million The U.S. dollar principal belongs to the limited partners. Peak XV has reduced its spread to 20% from the previous 30%.

The cuts will occur in Peak XV’s growth fund, which supports late-stage startups (after Series A), as opposed to seed and venture funds. “The fact is that when our cost of capital is higher than other companies, it actually makes us uncompetitive. It puts us at a disadvantage,” said Shailendra Singh, managing director, now global head of Peak XV. “But even after changing that, we still have the best economics in the industry – 2 (management fees) and 20 (arbitrage) being the base case,” he asserted.

Asked whether this was a result of Peak XV losing the premium and brand value that comes with the Sequoia brand, the venture capital leader insisted that brand value should not come at the expense of making the fund less competitive. “Brands should be earned, not given. Sequoia is a specific brand, a great brand. By the time we separated, we had earned enough brand value,” said Singh, referring to its portfolio More than 40 companies have revenues in excess of $100 million.

Return LP funds

It’s almost unheard of for a venture fund to return capital to limited partners rather than invest it, so the $465 million reduction in its current fund is another surprise. Why reduce fund size when the market is attractive? “This is a rare event. Despite the funding cuts, we remain one of the largest growth funds in India,” Singh said.

Peak Any pressure. Funding has been raised over decades.

However, one venture capital executive who spoke on condition of anonymity to speak freely told Mint There is more to do. “While the market was overheated, in the case of Peak XV, their primary sponsor, Sequoia Capital, no longer existed. So, they had to give the money back. Sequoia was a fundraising genius, and Peak XV was not,” he explain.

However, Singer insisted that anyone with a 10- to 20-year view would know that the reduction in fund size is not significant. “These funds were sized during the investment boom in late 2021 to early 2022. The reality today is that Indian public markets are doing well and companies of all growth stages are looking to earn the same P/E multiples. Plan based on current public market multiples and Not a prudent strategy,” he said, alluding to the founders’ high valuation expectations. “India is a hot market right now, but Southeast Asia might be a better option at a time like this. We definitely don’t want to trade at 50-60 times Ebitda.”

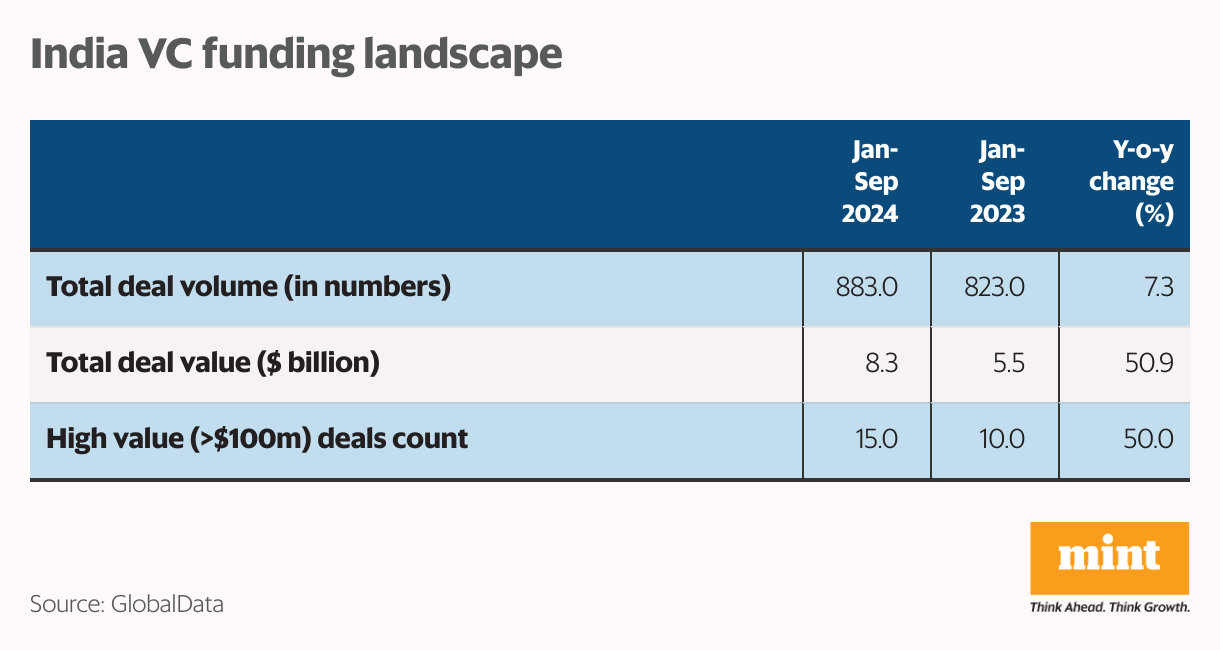

Despite Peak XV’s caution about growth-stage investments, Indian startups raised $7.5 billion in venture capital funding across 780 deals between January and August 2024.

The founders hope to raise capital at a much higher valuation multiple than Peak XV is willing to agree to. The founders expect to raise funds at a valuation equal to 40 to 60 times their revenue.

Peak XV is concerned about expectations for the small-cap market, which it believes is particularly overheated (its founders expect valuations of $500 million to $1.5 billion) because many companies don’t have the sales or users to justify such valuations . For venture capital funds, seed investments typically range from $25 million to $100 million.

“Our growth team chooses not to pay public market multiples for private companies,” Bhatnagar explained. “As stewards of other people’s (limited partners’) capital, our job is to stay disciplined and play out the cycle.”

Despite Peak , transaction volume increased by 5.1%. That’s according to London-based analytics and consulting firm GlobalData.

During the same period, India accounted for 7.3% of global venture capital deals and 4.6% of total financing. While this is a big improvement compared to the long funding winter of the past two years, it is still below the peak of 2021 when Indian startups raised huge funds.

Some of the key VC deals that took place in India between January and August include fast commerce company Zepto raising $665 million and $340 million in two separate funding rounds, marketplace Meesho raising $300 million, online pharmacy PharmEasy raising $2.16 hotel chain OYO raised $1 million, and renewable energy company Radiance raised $150 million.

solid foundation

Sequoia Capital was founded in 1972 by Don Valentine, who had previously co-founded Fairchild Semiconductor in Silicon Valley. It has backed many of today’s biggest names, including Apple, Google, Airbnb, Zoom, Nvidia, WhatsApp, Stripe and ByteDance, demonstrating its ability to identify, support and nurture high-potential startups.

In 2006, the company opened an India office, headed by Singh, who was living in the United States at the time. GV Ravishankar, who now heads the growth fund, joined at about the same time as Bhatnagar. By early 2025, the three MDs will have completed their 19-year terms together.

Peak XV has a team of over 100 employees, including 12 Managing Directors (General Partners), with Rajan Anandan leading the seed fund Surge and Bhatnagar leading the venture fund (Series A) or early-stage investments.

Recently, the brand’s portfolio companies have suffered a series of fires (Peak XV is not the only investor in these companies), including BharatPe, Zilingo, Trell, Byjus and GoMechanic. The governance of most of these companies was found to be flawed. Some founders admitted financial irregularities, and Trell was found to have inflated its user numbers.

“We have taken a lot of steps to ensure that this type of problem does not reoccur in the future,” said Singer, who has served on Sequoia Global’s board of directors for 12 years, listing various measures. The broader venture capital world has even tightened disclosure norms. Early companies are trying to prevent more of these incidents from happening.

Betting on Niche Games

Today, Peak XV is focused on supporting three themes: artificial intelligence (AI), fintech and consumer. It also opened an office in the United States for cross-border transactions.

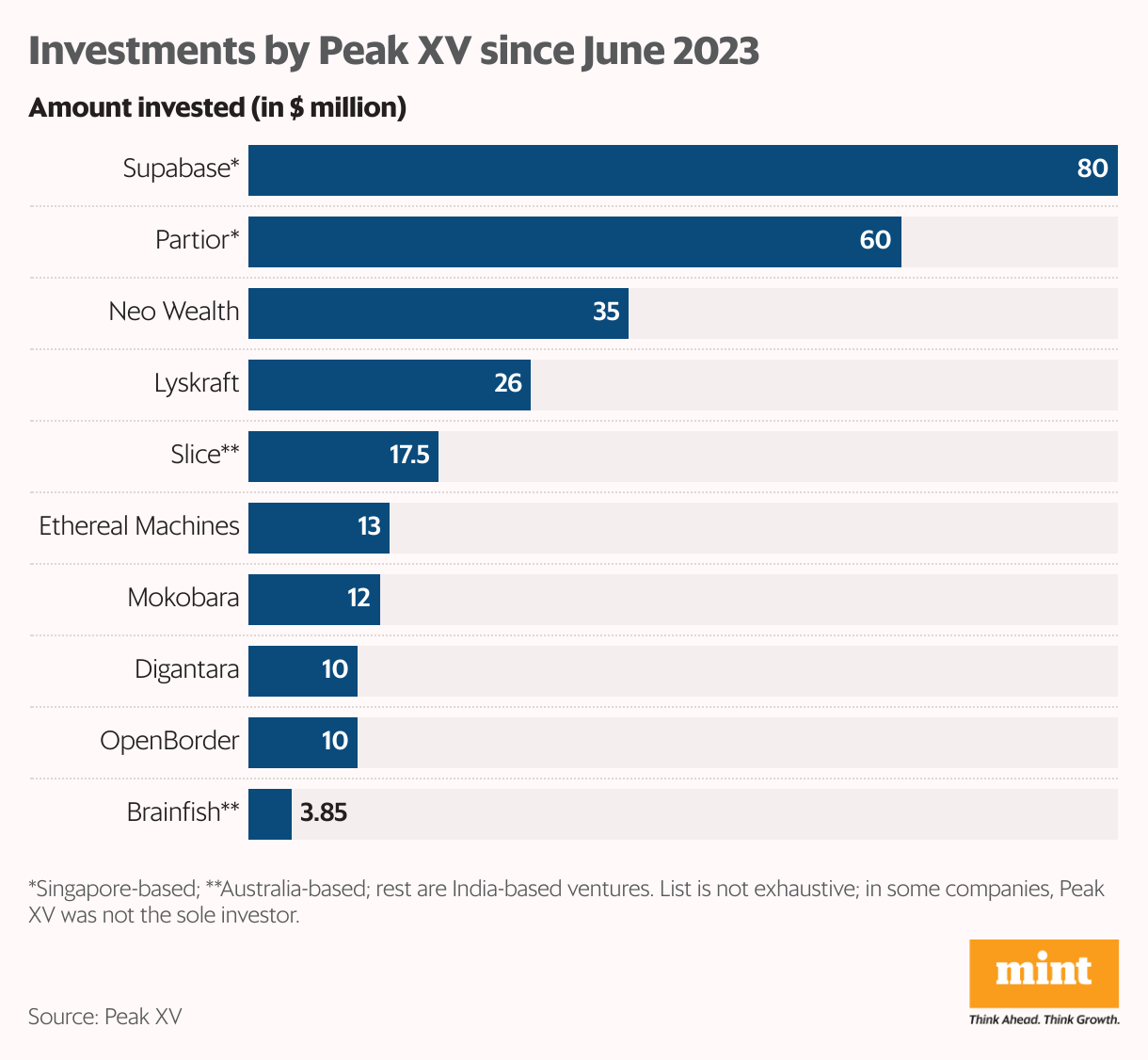

Despite its high valuations, Peak XV has invested in five growth-stage businesses in the past 12 months, including social commerce marketplace Meesho, jewelry retailer BlueStone, NBFC Neo Wealth and Singaporean open-source development platform Supabase, which in 2017 Raised $80 million. Series C financing in September (led by Peak XV and Craft Ventures).

India remains a price-sensitive market and Peak XV is looking at ideas to reduce costs and tap into the next tier of the market. For example, Patta Nagar is eyeing businesses that can provide low-cost medical services ( $100 to $300 price points), scale. He believes that, as is the case in the telecommunications industry, once prices fall, new competitors cannot easily enter, and the scope of competition for existing competitors will only expand. He should know because he briefly worked at Bharti Airtel before joining Sequoia Capital.

Peak XV prefers seed investments, venture capital and exits. Seed investment company Surge launched its tenth batch of products on October 22. In the consumer sector, the focus is on high-end brands. For example, it’s considering businesses like direct-to-consumer luggage brand Mokobara, which raised $12 million in a funding round led by Peak XV Partners in February at a valuation of $80 million. With millions of new passports being issued each year, peak XV expects the number of travels to surge and the number of creative ideas targeting this segment to continue to grow.

In the AI space, Peak XV is interested in ideas like Sarvam, which focuses on voice-centric AI solutions in India. As for the fintech space, which already has over 2,000 startups, it sees more niche players and untapped space. There are also a number of secondary opportunities and sub-categories, such as supply chain financing, which Peak XV will evaluate, Bhatnagar said.

As for the future, he said: “We are thinking about expansion, not contraction. We are also hiring in the United States to enable cross-border transactions.”

Follow us On Social Media Twitter/X