2024-10-28 18:59:26 :

Ratan Tata faced many challenges after taking over. One of the questions is: Can the group survive the competitive onslaught of the neoliberal economy?

Thirty years later, even though India’s economy has grown some 13 times and many other business groups that dominated India’s corporate landscape in the 1990s have fallen behind, the Tata Group remains a behemoth. According to data from the CMIE ProwessIQ database, Tata group companies accounted for 6% of India’s corporate assets in 2023, down about one percentage point from 30 years ago.

While Tata Group has retained its share, other groups have led the way. Mukesh Ambani’s Reliance now accounts for 9.6% of corporate assets, well ahead of the group they were second to 30 years ago. In terms of revenue, the gap between the two is even closer, with Reliance Group accounting for 6.3% of the overall revenue of the private enterprise sector, while Tata Group accounted for 5.2%.

View full image

Other groups have not been as successful in terms of growth, at least relatively speaking. Take Larbai Group as an example. In 1995, its assets ranked 10th. By 2007, the group had fallen out of the top 50 corporate groups by assets. Videocon and its group companies were ranked 13th in terms of assets in 1995, but by 2023, they were ranked 50th.

The ProwessIQ database used in this article excludes banks (public and private), government companies and public sector units, and conglomerates dominated by financial companies (such as Peerless or Sahara). The figure is adjusted for changes in company ownership, acquisitions and divestments; it does not reflect adjustments for investment within the group, which ideally should be netted out to get a better understanding. Data from 2023-24 is also excluded.

Beyond the dynamics of individual groups and the rise and fall of family businesses across multiple industries, what’s the bigger picture? How are “traditional” business groups faring in an era of huge upheaval in the Indian and global economies?

ruling family

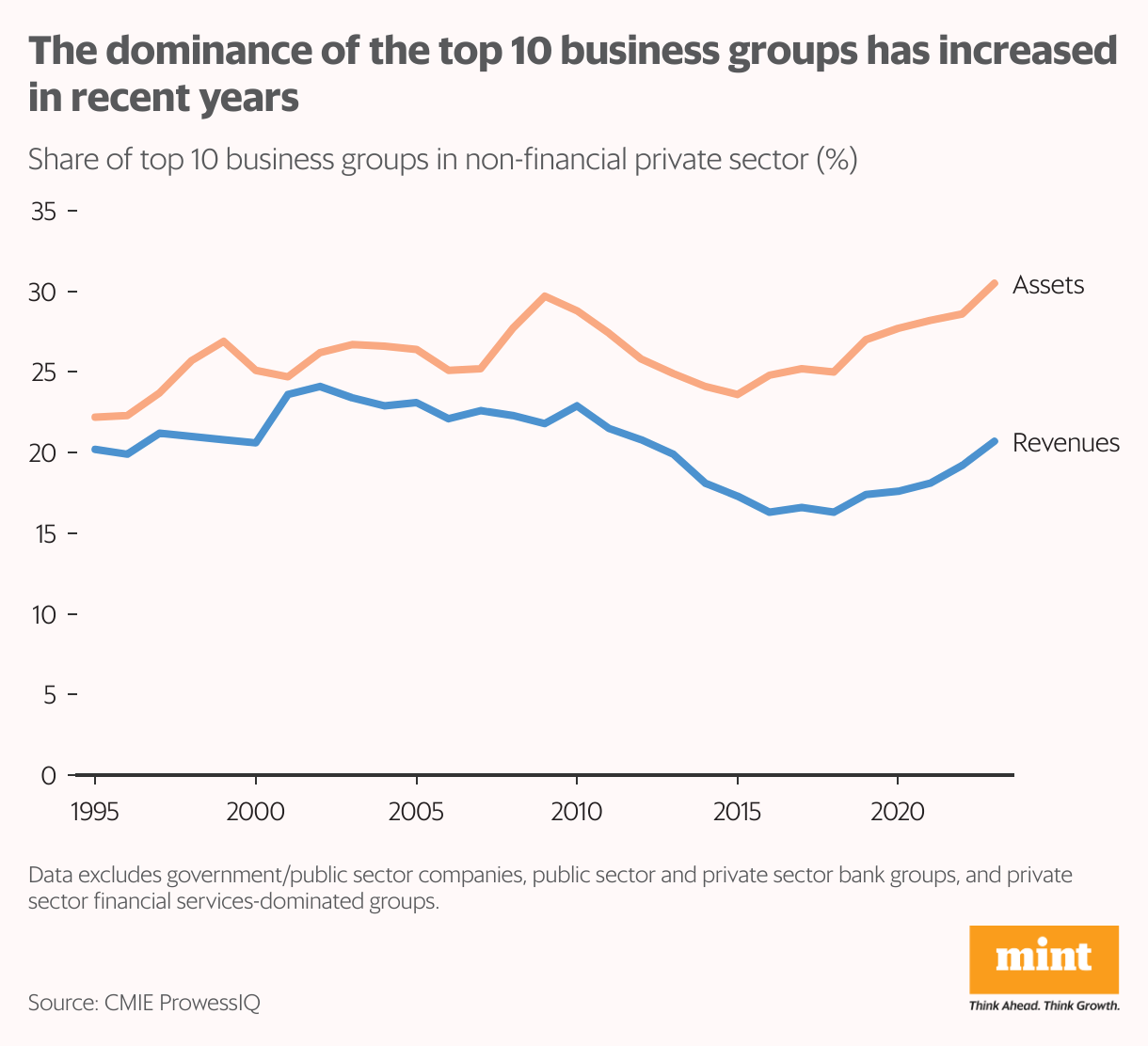

Despite the relative rise and fall of business groups, many of the largest groups in 1995 are still very well-known today, including Aditya Birla, RPG, Bajaj, Larsen & Toubro (L&T), and others. In 2023, the top five business groups by assets are Reliance, Tata, Aditya Birla, Adani and L&T. By 2023, the top 10 conglomerates will account for 31% of assets, up from 22% in 1995. Among the top 10 conglomerates, only L&T can be described as non-family controlled (see chart).

What about the turnover of the top 50 business groups? A 2007 study surveyed family businesses around the world, compiling data on India’s top 50 conglomerates by assets since 1939. According to the study, between 1939 and 1969, 32 new groups entered the top 50 list, and an additional 43 groups entered the top 50 business groups. The year 1997, 30 years ago, does not appear on the list.

If liberalization had indeed succeeded in dismantling existing firms, introducing competition, and loosening barriers to entry in a range of industries, turnover should be as high as in 1997, if not higher. But according to ProwessIQ, only about 30 of the top 50 groups by assets in 2023 did not appear on the 1997 list.

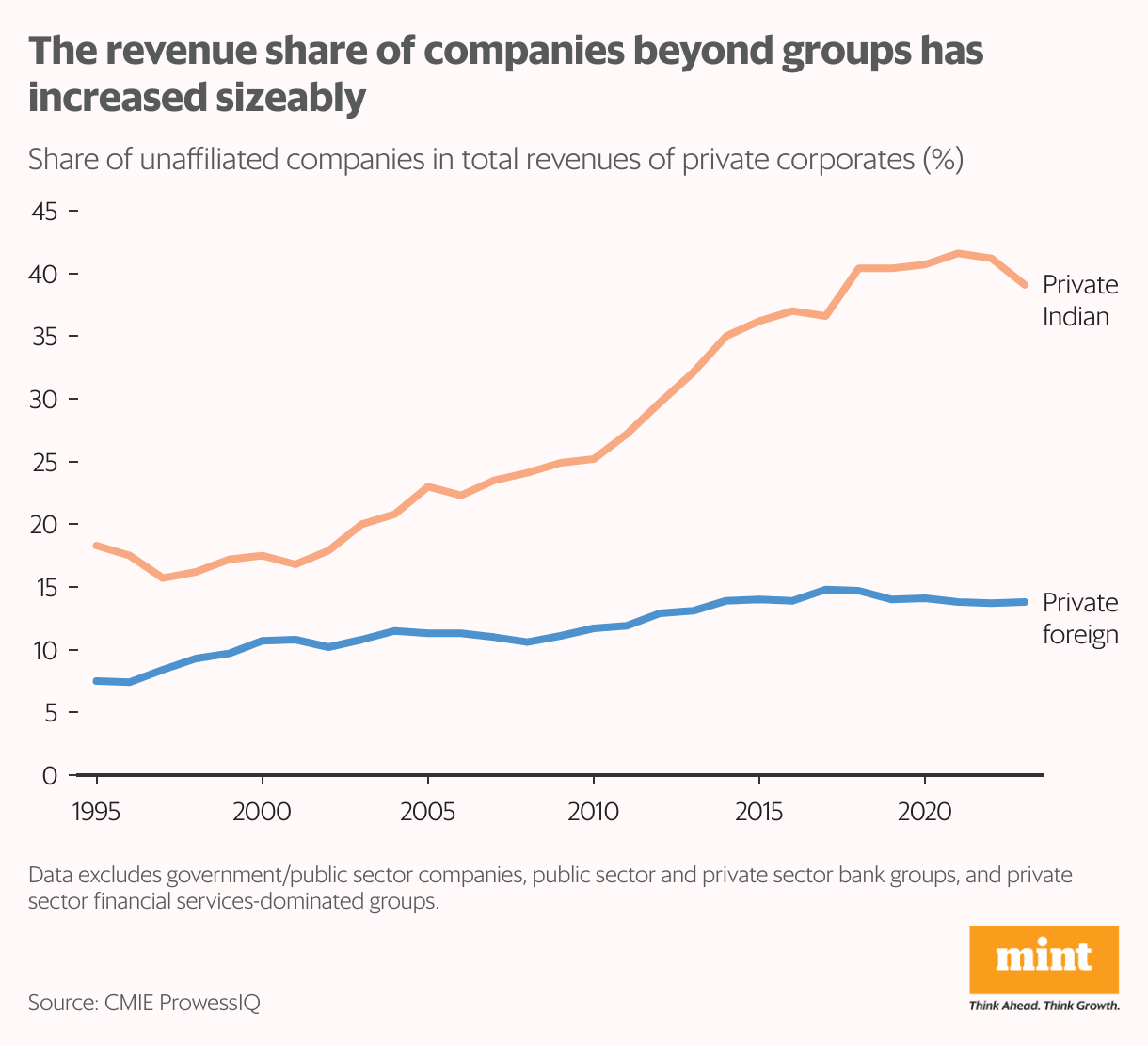

Things change when we focus on revenue rather than assets and add “unaffiliated” companies. These are companies like Infosys that are not part of any conglomerate in the Prowess database. By 2023, such companies will account for nearly 40% of non-financial corporate sector revenue, up from just 18% in 1995. Furthermore, it is interesting to note that the share of foreign companies in total revenue rose to 14% around 2014 and then remained flat. Then it was closed. Even in terms of assets, the proportion of non-related domestic enterprises has increased from 17% in 1995 to 28% in 2023.

However, since 2015, although the proportion of non-related domestic enterprises in total revenue has continued to grow, it has gradually stabilized. Starting around 2017, the share of total revenue accounted for by the top ten business groups has increased by about 4-5 percentage points to about 21%, which is roughly the same level as in 1995.

Group strength

How should we view the growing importance of independent firms since the 1990s relative to the dominance of conglomerates in the pre-liberalization era? Part of the story is that during the licensing period, established business groups had an advantage in obtaining credit and industrial licenses from the government and state-owned banks because of their political connections. Therefore, one of the main reasons why business groups dominate is rent seeking. Overall, they’re just better at managing it.

View full image

Furthermore, in a controlled economy, these groups can allocate scarce credit and capital, human and technological capabilities to promote business in their strong growth industries. As Tarun Khanna and Yishay Yafeh noted in a 2007 paper: “If diversified groups can compensate for the institutional deficiencies associated with the entrepreneurial process, they may Will be efficient: New ventures launched by conglomerates not only rely on the conglomerate’s capital infusion, but also on the conglomerate’s capital infusion, which is often reflected in the group’s brand name and its reputation, providing a rare guarantee in emerging markets. . There is also an internal (within-group) talent market. In this sense, some business groups may be closer to private equity firms than conglomerates. “

The difference is that, generally speaking, commercial groups have much longer investment horizons than the average private equity firm. Ironically, many analysts have long been critical of precisely this attribute of large conglomerates—their tendency to spread themselves out into many unrelated business areas and have no “focus.”

After 1991, as markets became relatively more accessible, talent, skills and capital found it easier to build profitable independent companies rather than companies affiliated with business groups whose interests might be owned by the family running the group rather than The manager or worker gets to actually run it. Funding sources such as foreign investment have become more diverse and widespread, as have technical and managerial talent. Graduates from top management schools no longer default to established business groups.

In a controlled economy, large business groups can allocate scarce credit and capital to boost their businesses in industries with strong growth.

Of course there are limits to this. One possible reason for some degree of recovery among conglomerates in the second half of the 2010s is the credit crunch faced by Indian industry. Banks hit by severe NPAs have turned cold towards the corporate sector. In such an environment, large groups with mature businesses have a natural advantage in obtaining the credit that banks are willing to extend. But overall, in order to survive, traditional conglomerates must move more nimbly and faster to stay in the competition.

Industry Picks

In the long run, successful groups are those who have the foresight or are lucky enough to be in businesses that will take off after the 1990s. The most striking example is the Tata Group’s decision to form Tata Consultancy Services (TCS) in the 1960s. By 2023, TCS has emerged as the crown jewel of the group. Reliance’s foray into refining has proven lucrative over the past few decades, providing the group with cash to expand into new businesses, from retail to telecoms to media.

View full image

Other groups are not expanding into newer “growth” areas at the same pace. Take Larbai Group as an example. In 1995, 45% of the group’s revenue came from textiles. The industry remains the group’s biggest cash cow by a wide margin in 2023, amid fierce competition globally. A study that goes against this is that of the Tata Group. In 1995, steel and commercial vehicles were the Tata Group’s main sources of revenue. By 2023, these two industries, while still important, will be second only to software.

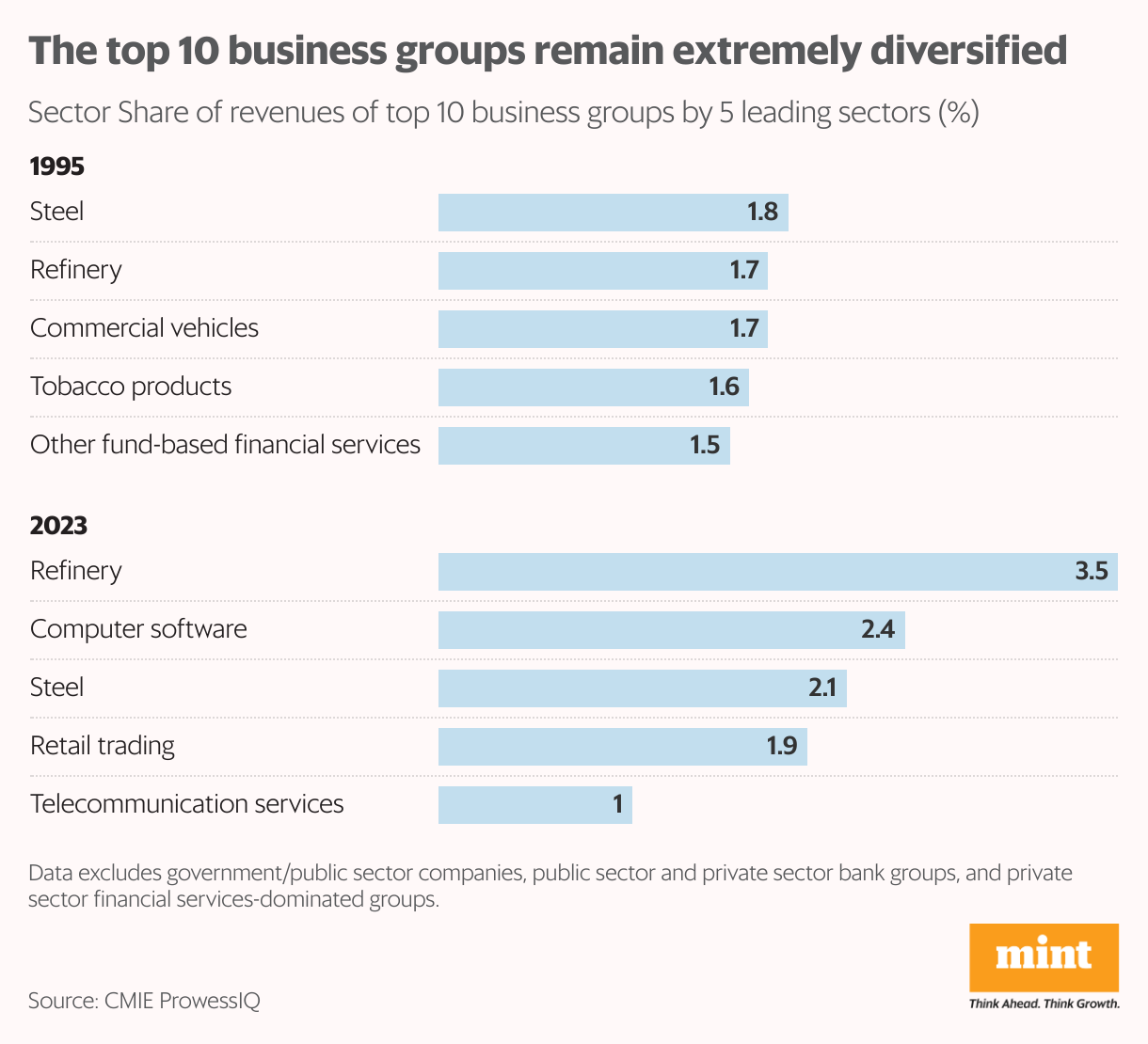

Interestingly, while for individual groups (such as Tata Group or Reliance Group) a single industry, refinery or software may account for a large portion of revenue, for the entire top 10 groups, revenue by industry Not particularly highly concentrated. This shows that even today these groups remain highly diverse (see chart).

What about non-affiliated companies? In 1995, these companies derived most of their revenue from “wholesale trade.” This remains unchanged in 2023. But by 2023, industries that were not important to these companies in 1995 dominate – software and IT services, retail and automotive accessories.

Conglomerates that maintained their ranking were also more aggressive in acquiring new businesses and divesting old ones. The CMIE database records changes in company ownership and tracks changes in a company’s cross-group or “unaffiliated” status.

While not all such ownership changes are necessarily acquisitions or divestments, surprisingly the largest groups also see high levels of turnover in companies in and out of the group. For example, since 1993, 99 companies have exited the Tata Group, while 140 companies have entered the Tata Group.

In the case of Adani, 11 companies left the group while 84 companies joined it. After the split of Ambani Group companies among the brothers, 28 companies left Mukesh Ambani Reliance Group while 183 companies joined the group (a considerable number of them were in the Adani Group). Following the acquisition of DEN Networks in 2018, the cable TV business will be launched in 2020).

Ultimately, if the past 30 years of turmoil in India’s industry are any guide, the largest business groups aren’t going away anytime soon. They will likely continue to rule. Smaller businesses will face pressure to grow or stagnate.

howindialives.com is a public data search engine.

Follow us On Social Media Twitter/X